Sparta&Athens_ATM.pptx. Lépontiens. Germany finds historic parallel for opting out of QE - MarketWatch. LONDON (MarketWatch) — The stage may be about to be set for a rerun of a shadowy episode in monetary history under which the German Bundesbank brandished an opt-out from support for weaker central banks on the European currency scene.

The exemption was contained in a secret agreement in November 1978 between Otmar Emminger, then-Bundesbank president, and Helmut Schmidt, German chancellor, a document subsequently known to central bank historians as the Emminger Letter. Draghi would be uncomfortable about engineering a legal confrontation with the Bundesbank that he could lose.

In Rome on Sept. 11, 1992, Carlo Azeglio Ciampi, governor of the Banca d’Italia, was called to the telephone to be told of the Emminger letter, under which the Bundesbank was entitled to stop intervening to support the lira, during crisis consultations with Giuliano Amato, Italian prime minister, and Piero Barucci, finance minister. Ciampi returned to the meeting “pale, almost white,” according to Amato’s account. Reparationsforderung: Griechenlands 476-Millionen-Anleihe gibt es nicht - D. This article is from the November/December 2009 issue of Dollars & Sense: Real World Economics available at This article is from the November/December 2009 issue of Dollars & Sense magazine.

By Alejandro Reuss. Economic Principals » Blog Archive » Economics in the Next Ten Years? A young economist, or an economics journalist interested in what the young are working on, could do a lot worse than reading through, as I did the other day, 55 very short papers written by distinguished economists describing the large questions they think are likely to dominate the next generation of research in their respective fields.

They are among 252 papers by experts in various disciplines who responded to an invitation by the National Science Foundation’s Directorate for the Social, Behavioral and Economic Sciences to describe “grand challenge questions” that transcend near-term funding cycles, questions which therefore might benefit from investment in infrastructure. From the response, this much is immediately apparent: interest in financial crises, medical systems engineering and, perhaps above all, new instrumentation share pride of place at the top of the list. A golden age of evidence-based economics lies ahead, thanks to the computer and the Internet. Turmoil sends investors scrambling for havens - FT.com.

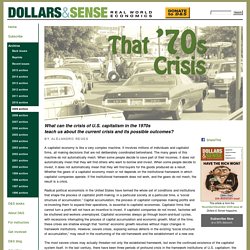

Investors At Davos Feared 1994 Moment - Business Insider. Was ist Zionismus? Black Gold: The End of Bretton Woods and the Oil-Price Shocks of the 1970s. The "Lehman" Moment. Via Peter Tchir of TF Market Advisors Lately it is hard to avoid talk about the Lehman "Moment".

It almost makes you think that the world fell apart the weekend Lehman filed for bankruptcy protection. 50/50 Chance of US Lapsing Back Into Recession: Economic Historian. US Government has previously defaulted, it’s not risk-free. The US Government is teetering toward another debt ceiling crisis, and it is useful to remember that failing to make repayments on government debt is not new for the US.

The US Treasury defaulted three times on its treasury bills in 1979, when Congress didn’t legislate in time to raise the debt ceiling. In 1979, they were ‘temporary’ defaults, and they were rectified within a month, but they did shock people who believed that the mighty US government would always pay its debts on time. Since the Mexican debt crisis, 30 years of neoliberalism. Mexico’s collapse of 1982, and the extreme response of the US and IMF, marked the birth of an elite consensus that continues to haunt Europe today.

As Nick Dearden, Director of the Jubilee Campaign for debt cancellation just wrote for the New Statesman, this week marks the “anniversary of an event of great resonance”. For this week it is exactly 30 years ago that Mexico temporarily suspended its debt payments to foreign creditors, thereby marking the beginning of what would eventually escalate into the first international debt crisis of the neoliberal era. Things would never be the same again.

What ensued was not only a tragic collapse of living standards throughout the developing world and a lost decade for Mexicans and millions of poor people in the Global South – most notably in Latin America, Eastern Europe and Africa — but also a historic shift in power relations between debtors and creditors in the emerging global political economy. Dollar Faces the Market’s Judgment on a S&P Downgrade to AA Monday. Dollar Faces the Market’s Judgment on a S&P Downgrade to AA+ Monday Euro Sovereign Debt Troubles Worsen as the ECB Scrambles to Offer ReliefSwiss Franc Looks an Ideal Safe Haven for Capital that May Flee the USJapanese Yen Intervention was for Not if a Financial and Dollar Crisis Sweeps the MarketAustralian Dollar Outlook Mixed as Market Weighs Risk and US Dollar Waves Gold the Primary Benefactor for Anti-Dollar, Anti-Currency Sentiment Dollar Faces the Market’s Judgment on a S&P Downgrade to AA+ Monday Though the dollar was already trading under heavy fundamental waves through the past week; the coming week will likely see the swells turn into a tidal waves wave starting with Monday’s Asian open.

With the backdrop already roiled by a building global financial crisis; US market conditions took a serious turn for the worst after the close on Friday. When it comes down to it, this move was not unexpected. Euro Sovereign Debt Troubles Worsen as the ECB Scrambles to Offer Relief. Macro and Other Market Musings: Repeating the Fed's Policy Mistake of 1936- Is the Federal Reserve (Fed) making a similar mistake to the one it made in 1936-1937?

If you recall, the Fed during this time doubled the required reserve ratio under the mistaken belief that it would reign in what appeared to be an inordinate buildup of excess reserves. The Fed was concerned these funds could lead to excessive credit growth in the future and decided to act preemptively. What the Fed failed to consider was that the unusually large buildup of excess reserves was the result of banks insuring themselves against a replay of the 1930-1933 banking panics.

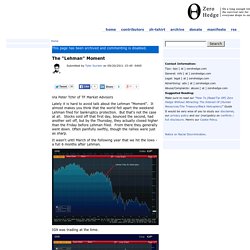

So when the Fed increased the reserve requirements, the banks responded by cutting down on loans to maintain their precautionary level of excess reserves. As a result, the money multiplier dropped and the money supply growth stalled as seen in the figure below. The EM’s ‘fragile 8′ must save themselves. On macroeconomics A blog on macroeconomics, economic policymaking and the financial markets.

Gavyn usually writes about a key topic of the week on Sunday. Paul Krugman on France (1990-2010): Long live the franc, long live the Fren. This post covers Paul Krugman’s views on France between 1990 and 2010 as expressed in his public, non-academic writings.

Knowing the champion of American liberalism’s past views helps place his current criticism of the euro crisis in context and highlights similarities and differences with European progressives. These views can be summarized: MMT, The Euro and The Greatest Prediction of the Last 20 Years. By L. Randall Wray Lest you think NEP is tooting its own hyperbolic horn a bit too much, I borrowed the title of this post from a 2011 piece written by someone who is currently hostile to MMT even though he acknowledges its predictive accuracy. (I’ll send 5 Buckaroos to the first person who can identify the author! Sorry, UMKC students are not eligible—they have to work an hour for each Buckaroo to pay their taxes.) The author of that original piece went on to provide some proof for the case he was trying to make. 010_HISTORY_GBP-CHF.pdf (application/pdf Object) 010_HISTORY_CHF-YEN.pdf (application/pdf Object)

Related Charts(Click any thumbnail image to view the full-sized interactive chart) Compares core CPI, headline CPI, PPI Finished Goods and PPI All Commodities back to 1968. Series are compared using a 12 month percentage change. The goal of the core CPI is to remove the most volatile cost-push components of the headline number. This creates a series that indicates whether short-term commodity price changes are resulting in... This chart illustrates the effect inflation had on the perceived returns of the Dow Jones Industrial Average during the 1970s. Amazon.com: Der Frankenkurs des Dollars 1973-1980: Ein Test der Kaufkraftpa. Worst Hyperinflation Episodes In History - Business Insider. Friedman, Schwartz - A Monetary History of the United States.pdf (applicati. A Brief History of Regulations Regarding Financial Markets in the United St. NBER Working Paper No. 17443Issued in September 2011NBER Program(s): DAE In the United States today, the system of financial regulation is complex and fragmented.

Responsibility to regulate the financial services industry is split between about a dozen federal agencies, hundreds of state agencies, and numerous industry-sponsored self-governing associations. Regulatory jurisdictions often overlap, so that most financial firms report to multiple regulators; but gaps exist in the supervisory structure, so that some firms report to few, and at times, no regulator. The overlapping jumble of standards; laws; and federal, state, and private jurisdictions can confuse even the most sophisticated student of the system.

This article explains how that confusion arose. The Economy of God - Wikipedia, the free encyclopedia. The Economy of God, first published in 1968, is one of Witness Lee's principle works and is a compilation of messages he gave in the summer of 1964 in Los Angeles. These messages build on one of Watchman Nee's classics, The Spiritual Man, which reveals that man is composed of three parts-spirit, soul, and body. The Economy of God shows how this understanding of the parts of man tie into the central revelation of the Bible, which is God's economy, God's plan to carry out His heart's desire of imparting Himself into man for His full expression. Global bond demand, by source, 2007-2014(est) finance.yahoo.com/news/most-i. Macro and Other Market Musings: Repeating the Fed's Policy Mistake of 1936- ▶ The Ascent of Money: A Financial History of The World by Niall Ferguson E.

Last days of the USSR - FT.com. The roles of Gorbachev and Yeltsin in the coup that led to the collapse of the Soviet Union remain elusive August 19 1991: tanks in Red Square he coup began on a hot Sunday afternoon. Shortly before five o’clock on August 18 1991, five black Volga cars arrived at the gates of Foros, the holiday retreat of the president of the Union of Soviet Socialist Republics, Mikhail Gorbachev, on the Black Sea coast of Crimea. No one was expecting them, and the guards did not initially open the gates or remove the chains of tyre puncture spikes lying across the road. Then General Yuri Plekhanov, the head of the ninth directorate of the KGB, stepped out of the first car. Die Schatzbildung ging zu Ende. Tallyjuly2009.pdf (application/pdf Object) www.cfapubs.org/doi/pdf/10.2469/faj.v68.n6.1. Swiss Central Bank Faces Tough Choices at Meeting: Analysts - CNBC. Guest Post: Charting The Federal Reserve's Assets - 1915-2012. Breakingviews.com - To Treat the Fed as Volcker Did - NYTimes.com.

Sober Look: As spring approaches, will the corporate sector expansion peak. Short-Selling Ban History Lesson: Sept. 19, 2008. 1931 - Weltwirtschaftskrise und globale politische Instabilität - chronikne. Of Kiwis and Currencies: How a 2% Inflation Target Became Global Economic G. Global Imbalances and Low Interest Rates: - BISwpCmtsCaballeroFG-AuCISENR.p. United States invasion of Panama. JAPAN ECHO - FOREIGN POLICY AFTER KOIZUMI Vol. 33, No. 4 - Japan as an Inve.

Debt and Growth in the G7 - NYTimes.com. www2.econ.iastate.edu/tesfatsi/luccrit.pdf. 1990-92 Early 1990s Recession - Timeline - Slaying the Dragon of Debt - Reg. Der Weg zur Immobilienblase « Never Mind the Markets. Inflation: The Cost-Push Myth - Inflation_Jun_Jul1981.pdf. Cultura di Golasecca. The Joseph Cycle by Simon Sim. Principality of Seborga - Wikipedia, the free encyclopedia. Economic Principals » Blog Archive » Economics in the Next Ten Years? 50/50 Chance of US Lapsing Back Into Recession: Economic Historian. Whatever Happened to Inflation? - Reason.com. Black Gold: The End of Bretton Woods and the Oil-Price Shocks of the 1970s. RBA: Bulletin February 2001-Statement on Monetary Policy. Germany finds historic parallel for opting out of QE - MarketWatch. Reparationsforderung: Griechenlands 476-Millionen-Anleihe gibt es nicht - D. Public Sector Employment. Investors At Davos Feared 1994 Moment - Business Insider. Turmoil sends investors scrambling for havens - FT.com. Insights From The Most Successful Investors In History.

The "Lehman" Moment. Aurelija Augulyte sur Twitter : "Collapse of UK as we know it... Origins and Destinations of the World’s Migrants, from 1990-2013. Are we starting to see why its really the exorbitant “burden” Are We Starting To See Why It's Really The Exorbitant 'Burden' Patrick Chovanec sur Twitter : "Whose population is growing, and whose isn't: Haq's Musings: India's Rising Population and Depleting Resources. We are trapped in a cycle of credit booms. Rafael Domenech sur Twitter : "EZ core inflation down to 0.8% and all countries below 2% despite differences in U rates.

Mark J. Perry sur Twitter : "CHART: History of US Highest Marginal Income Tax Rates, 1913 to 2013... Remember the paranoia about inflation? It’s dead, almost everywhere. Is the Strong Dollar Sustainable? Anuar D. Ushbayev sur Twitter : "@DorganG @wonkmonk_ @stf18 late Fischer Black comes to mind & the concl. par. of his '86 Noise. Minority Of One sur Twitter : "Milton Friedman's stay in 1960s India. 2014's India is no different. #NREGA cc: @ScrewedbyState. Immigrant entrepreneurs power U.S. economy. Most Efficient Health Care Around the World. Mussolini’s great monetary policy failure. Capital Controls May Make Economic Sense, Minneapolis Fed Paper Says - Real Time Economics.

George Dorgan sur Twitter : "@MaMoMVPY @SFait79 @acemaxx Money up, Assets up, sentiment up, spending up, HH savings rate down #BrettonWoods2. The fall of the Berlin Wall and the end of global extreme poverty. Stop Worrying About 'Currency Wars' Ninja Economics sur Twitter : "Current oil crash mirror of 08 oil pop h/t @EMostaque. Dallas Fed sur Twitter : "World output growth slowed to 2.8 pct. YOY in Q3. More: Nero sur Twitter : "150 years of global monetary policy summed up in one chart... Nighttime Must-Read: Nouriel Roubini: Where Will All the Workers Go? - Washington Center for Equitable Growth. Aurelija Augulyte sur Twitter : "stating the obvious... [2/100] Economic World History in One Chart. Max Roser sur Twitter : "Economic World History in One Chart Chart 2 of 100 – World Income Distribution over 200 years.

Six Things Technology Has Made Insanely Cheap - Bloomberg Business. Conrad Hackett sur Twitter : "PCs are now 99.9% cheaper than in 1980. The History of the Swiss Balance of Payments.