M.B.A. Programs That Get You Where You Want to Go. With some 13,000 graduate schools of business across the globe, the M.B.A. degree has clearly become a commodity.

Even among elite schools, courses and case studies are pretty much water from the same well (i.e., finance, operations, marketing, accounting). So how do you choose? By using the rankings? Which ones? The Economist’s? Don’t ask us. Conventional wisdom will tell you that Harvard is for Fortune 500 jobs, Wharton for Wall Street, Kellogg for marketing and Insead for multinational entities. Photo To Work at Amazon Go to Ross School of Business (University of Michigan) This might come as a surprise: Amazon regularly hires more M.B.A.s from top-10 business schools than big Wall Street firms.

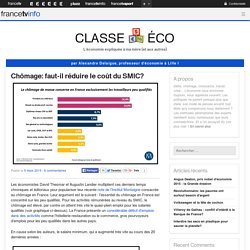

Marché du travail : la grande fracture. Chômage: faut-il réduire le coût du SMIC? Les économistes David Thesmar et Augustin Landier multiplient ces derniers temps chroniques et éditoriaux pour populariser leur récente note de l'Institut Montaigne consacrée au chômage en France.

Leur argument est le suivant : l'essentiel du chômage en France est concentré sur les peu qualifiés. Pour les activités rémunérées au niveau du SMIC, le chômage est élevé, par contre on atteint très vite le quasi-plein emploi pour les salariés qualifiés (voir graphique ci-dessus). La France présente un considérable déficit d'emplois dans des activités comme l'hôtellerie-restauration ou le commerce, gros pourvoyeurs d'emplois pour les peu qualifiés dans les autres pays. En cause selon les auteurs, le salaire minimum, qui a augmenté très vite au cours des 20 dernières années : La première chose que cela inspire, c'est que cela ne nous rajeunit pas. Et si l'on peut reprocher beaucoup de choses aux politiques sur l'emploi, on ne peut pas dire qu'ils ont été sourds à ces arguments.

Roland Mack, le constructeur de manèges qui nargue Mickey. Le Monde.fr | • Mis à jour le | Par Pascale Krémer Europa-Park 2/3.

Ce sexagénaire allemand est le grand architecte du succès du parc d’attraction Europa-Park, géré comme une PME familiale et doté de manèges faits maison. Roland Mack semble avoir fait du pied-de-nez aux Etats-Unis un moteur de vie. « Nous avons un restaurant deux étoiles au Michelin. Parce qu’en Europe, on mange bien partout, même dans les parcs d’attraction », dit-il. Cofondateur et patron actuel du royaume de la souris Euromaus (qui ne va pas sans en rappeler une autre), au côté de son frère Jurgen, et avec l’aide de ses deux fils, cet ingénieur de 65 ans manie la comparaison anti-Disney avec l’assurance que confère un résultat commercial à trois chiffres — secrets. « Nous n’offrons pas que des manèges pour les ados, nous divertissons de 3 à 90 ans, et l’entrée adulte ne coûte que 42,50 euros ». Une entreprise florissante « J’ai eu raison. Les Français, ces voisins bienveillants.

Why are interest rates so low? Interest rates around the world, both short-term and long-term, are exceptionally low these days.

The U.S. government can borrow for ten years at a rate of about 1.9 percent, and for thirty years at about 2.5 percent. Rates in other industrial countries are even lower: For example, the yield on ten-year government bonds is now around 0.2 percent in Germany, 0.3 percent in Japan, and 1.6 percent in the United Kingdom. In Switzerland, the ten-year yield is currently slightly negative, meaning that lenders must pay the Swiss government to hold their money! The interest rates paid by businesses and households are relatively higher, primarily because of credit risk, but are still very low on an historical basis. Europe at a crossroads. Embroiled with the Greek crisis, European policymakers will soon have to step back and reflect on the broader question of the future of the Eurozone.

Before calling for an exit or, on the contrary, for further integration, it is worth pondering over the consequences of each option. Oversimplifying, one could say that there are two strategies for managing the Eurozone: the current one which builds on the 1992 Maastricht treaty and its Fiscal Compact update in 2012; and a more ambitious federalist alternative. Federalism would be my preferred arrangement, but I am not convinced Europeans are ready to do what it takes to make it work. The Maastrichtian approach infringes member state sovereignty only through the monitoring of public deficits and debts. The founding fathers were presciently concerned that an impending default of a particular country may trigger a bailout: hence the Maastricht Treaty enclosed both a debt limit and a “no bailout clause”.