6 tax-saving strategies for smart investors. Commentary by Jessica McBride, CFP®, CTFA Senior Financial Advisor.

Roth IRAs 2021: Know the Facts! As we start 2021, we can reevaluate and anticipate our financial objectives, income assumptions, and tax-efficient savings opportunities for the new year.

Whether you are actively employed and accumulating assets or distributing income in retirement, a Roth IRA can play a major role in your financial plan. Roth IRAs are becoming more popular as investment vehicles, and for good reason! These accounts can provide incredible growth potential, cash flow flexibility, and favorable tax treatment to and through retirement. If you want to demystify Roth IRA contributions, conversions, rollovers, and distributions, let us dig into the facts!

SEPP for early 401K Withdrawals. This article includes links which we may receive compensation for if you click, at no cost to you.

Reader question: Can I use my 401k to retire early and avoid the 10% 401k withdrawal penalty? – Jesse, Boston. How to Access Retirement Funds Early. I’ve written a lot about the benefits of tax-advantaged accounts and why they are especially beneficial for people planning on retiring early.

I’ve even created a real-time experiment to prove that utilizing tax-advantaged accounts is the best way speed up your journey to financial independence. What I haven’t done yet though is write a comprehensive post about all the ways you can access the money in retirement accounts prior to standard retirement age. Today, I plan to fill in that missing piece of the puzzle and also determine which early-withdrawal method is best for early retirees.

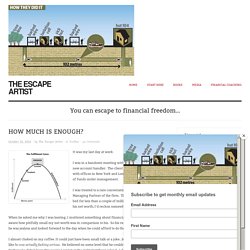

How much is enough? It was my last day at work.

I was in a handover meeting with a client to introduce the new account handler. The client was a private equity firm with offices in New York and London and a couple of billion of funds under management. I was treated to a rare conversation with the Big Cheese, the Managing Partner of the firm. The Top Eight Areas Where Millionaires Make Money Mistakes. RMD table from Fidelity. SECURE Act - HumbleDollar. Adam M.

Grossman | December 29, 2019 AS IF ON CUE, Ebenezer Scrooge recently showed up in Washington, DC. The result wasn’t pretty. A bill known as the SECURE Act, a favorite of the insurance industry, had been stuck in Congress all year. But suddenly, on Dec. 20, it got tacked onto another bill and signed into law. It’s the holiday season, though, so I’ll start with the few positive aspects of the law. Liz Weston: Who should consider a Roth conversion now? If you’ve saved a lot for retirement, or your parents have, you could be affected by recent changes in the rules about retirement distributions.

The recently enacted Secure Act eliminated the “stretch IRA,” a strategy used by affluent investors to pass tax-advantaged money to their heirs. The stretch IRA allowed nonspouse beneficiaries — typically children and grandchildren — to take money out of an inherited IRA gradually over their lifetimes. The new law requires most IRAs inherited by people other than spouses to be drained within 10 years, which can lead to much higher tax bills for heirs. 3 Monthly Dividend Stocks to Buy That You Can Rely On. We all have bills and expenses each and every month.

However, when it comes to investing in dividend-paying stocks, there’s always been a mismatch between when you get paid dividend distributions and when you cut checks or click to make your payments. This is because the vast number of U.S. -listed companies pay their dividends on a quarterly basis. And beyond the borders of the nation, many companies stretch out their distributions to bi-annual or even annual payments. Millennial Revolution Investment Workshop: A Step-by-step Guide to Investing ... You asked; we delivered.

Welcome to the Millennial Revolution Investment Workshop, a step-by-step guide to teach you how to invest from the ground up! How does it work? Right here in this space, we will be running a year-long workshop, using REAL money, in the REAL stock market, to show you exactly how to build your own portfolio of low-cost index ETFs, just like ours. And we will be there, every step of the way, to help you out and answer your questions. And the cost for all this? Retirement Seminar Notes + Discussion. The automatic millionaire summary. The Little Differences Between 401(k)s and IRAs Can Cost Big Bucks. 4 steps to make retirement less complicated. James McGlynn | August 7, 2019 YOU CAN THINK of retirement as having four phases.

Want to make sure you make the right decisions at the right time? An age roadmap can help. Phase No. 1 is the preretirement period beginning at age 55. 3 must do actions before leaving the workforce. Pass It On (IRAs) - HumbleDollar. Ross Menke | April 15, 2019 BABY BOOMERS are retiring every day and Generation X is right on their heels. With this, an increasingly large amount of wealth is making its way into IRAs and Roth IRAs, thanks to rollovers from employer retirement plans. I’ve found that many folks don’t quite grasp the complexities of such accounts.

On the surface, they seem pretty simple: You contribute to an IRA or Roth IRA, receive tax-deferred growth and then gradually withdraw the funds during retirement. Anything that’s left over after your death goes to the listed beneficiaries. If only it were so easy. Backdoor Roth - HumbleDollar. WHEN YOU CONVERT a traditional IRA to a Roth IRA, you don’t have to pay taxes on your nondeductible contributions.

Let’s say that, over the years, you have made $20,000 in nondeductible contributions to an IRA that’s now worth $30,000. When you convert, you don’t have to pay taxes on the $20,000 in nondeductible contributions. Thus, the conversion would potentially add just $10,000 to your taxable income, while giving you a $30,000 Roth that will grow tax-free thereafter. The funding of a nondeductible IRA, and then converting it to a Roth, is known as a “backdoor Roth”—a strategy that’s popular with high income earners who otherwise wouldn’t qualify to fund a Roth IRA.

Indeed, some high income earners do this every year, first funding a nondeductible IRA and then soon after converting it to a Roth. Best Money Tools. What Is the Rule of 55 and How Does It Affect You? The Ins and Outs of 401k Withdrawals at Age 55. Retirement Nest Egg calculator. Future Healthy: Using your HSA funds after age 65 - HSAstore.com. Life Expectancy per IRS: Publication 590-B (2017), Distributions from Individual Retirement Arrangements (IRAs) You must include early distributions of taxable amounts from your traditional IRA in your gross income. Early distributions are also subject to an additional 10% tax, as discussed later. If you were affected by Hurricane Harvey, Irma, or Maria, see chapter 3, Disaster-Related Relief. There are several exceptions to the age 59½ rule. Even if you receive a distribution before you are age 59½, you may not have to pay the 10% additional tax if you are in one of the following situations.

You have unreimbursed medical expenses that are more than 7.5% of your adjusted gross income. Most of these exceptions are explained below. Note. Distributions that are timely and properly rolled over, as discussed in chapter 1 of Pub. 590-A, aren't subject to either regular income tax or the 10% additional tax. For more information, see chapter 9 of Pub. 970. The additional tax on early distributions is 10% of the amount of the early distribution that you must include in your gross income. Compound Interest Calculator. Compound interest - meaning that the interest you earn each year is added to your principal, so that the balance doesn't merely grow, it grows at an increasing rate - is one of the most useful concepts in finance.

It is the basis of everything from a personal savings plan to the long term growth of the stock market. It also accounts for the effects of inflation, and the importance of paying down your debt. See How Finance Works for the compound interest formula, (or the advanced formula with annual additions), as well as a calculator for periodic and continuous compounding.

The Happiness Curve: Resources for the Voyage of Life. 11 Ways to Avoid the IRA Early Withdrawal Penalty. Withdrawing Money From an IRA Without Penalty. The Incredible Tax Benefits of Real Estate Investing. Here’s what you can learn from the last financial crisis that will help you with the next. Reasons-to-do-roth-ira-conversion-in-50s-or-60s-1. 9 Smart Ways To Withdraw Retirement Funds. How Much Money Will You Really Spend in Retirement? Probably a Lot More Than ... How to Optimize Your Journey to Financial Independence.

Traditional IRA vs. Roth IRA - The Best Choice for Early Retirement. Financial Planners. 401k Early Withdrawal Costs Calculator. Dreaming of an Early Retirement? Here’s What It Takes. How to Create an Emergency Binder for A Complete Disaster & Estate Plan - Mam... FIRECalc: A different kind of retirement calculator. How Not to Deplete Your Portfolio in Retirement - Millennial Revolution. How Much is TOO MUCH in your 401(k)? For all of its shortcomings, the traditional retire-at-65 system does have a few cushy benefits in the US. Flexible FIRE. Lessons from Millionaires - ESI Money. Eat your cake now or when you are 59.5? Addressing the conundrum. Note: My idea presented in this blog post appears to be fairly original and has received some recent attention in a popular finance podcast; learn more here.

My generation just rejects the idea of putting your head to the grindstone so you can golf and have a luxury hospital bed when you are old. We say: no. We want to enjoy life now. This means being frugal and investing, so we can develop a current stream of income now, and use that stream of income to pay bills, so we can work less. It’s a pretty simple formula, actually. Except, there is one large obstacle which has been tormenting me lately: the issue of IRA’s (individual retirement accounts). So, you might ask, why not simply avoid putting the money in retirement accounts, since it hides that money away until old age? How to Access Retirement Funds Early. Roth 401(k) Rollovers: Beware the 5 Year Rule - MBAF, CPAs and Advisors. How to avoid outliving your retirement savings. 10 Things I Didn’t Expect in Early Retirement. 10 Downsides to Early Retirement. The Negatives Of Early Retirement Life Nobody Likes Talking About - Financial...

12 ways to keep your brain young.