Judge Novack's Research Binder. Updated through Volume 436 of Bankruptcy Reports. 363 Finding New Ways to Sell Troubled Assets “Free and Clear” of Liens. One of the most effective vehicles for the rescue and revitalization of troubled business and real estate to emerge in recent years of Chapter 11 practice has been the “363 sale.”

Image via Wikipedia Named for the Bankruptcy Code section where it is found, the “363 sale” essentially provides for the sale to a proposed purchaser, free and clear of any liens, claims, and other interests, of distressed assets and land. Substantive Consolidation Law Review. A statutory basis for substantive consolidation? In re Cyberco Holdings, Inc., 431 B.R. 404 (Bankr. W.D. Mich. 2010) A popular line of thinking among bankruptcy practitioners and commentators holds that substantive consolidation – the combining of assets and liabilities of a debtor and another debtor or non-debtor entity to satisfy creditor claims against both entities ratably from the resulting pool – is an equitable remedy of judicial invention with no specific foundation in the Bankruptcy Code.

Many courts seem to agree with this view, with few even attempting to find a statutory basis for substantive consolidation outside of the court’s broad authority to issue orders under section 105(a) of the Bankruptcy Code. However, a recent Michigan bankruptcy court decision upsets this conventional thinking, finding statutory authority for substantive consolidation by combining provisions found in sections 542(a) and 502(j) of the Bankruptcy Code. Judge Jeffrey R. Hughes’ decision in In re Cyberco Holdings, Inc., 431 B.R. 404 (Bankr. Utility Revamps Debt to Aid Survival.

Bowman Gilfillan Attorneys. Dynegy Says It May Violate Credit Covenants This Year. Money Health Central - Personal Finance With A Twist. Latham & Watkins LLP - Firm Publications - The Impact of CDS on Restructurings. Empty Creditors. Preference Claims. Check Yourself Before You Wreck Yourself: Partial Involvement in a Bankruptcy Case May Cause Parties to Lose Protections Under the Bankruptcy Code. “When I believe in something, I fight like hell for it.” – Steve McQueen A recent decision from the Bankruptcy Court for the Eastern District of North Carolina illustrates the dangers inherent in overlooking one’s rights in bankruptcy.

Indeed, unintentional errors may cause creditors to lose sacrosanct protections that they would have been afforded had they simply stayed out of the case altogether. Creditors and other parties in interest should take care not to imply their “tacit consent” to actions taken in the bankruptcy case that would otherwise be denied sua sponte by the court. NACBA > Home. Pension Bill Irks Experts - Bond Buyer Article. WASHINGTON — As a House Judiciary Committee panel meets Monday to hold a hearing on public pensions and the need for state bankruptcy protection, pension and muni bond experts are opposing a recently introduced bill that would prohibit them from issuing tax-exempt bonds unless they subject their pension plans to federal oversight and regulation.

All of the witnesses slated to testify at the hearing — James Spiotto, a partner at Chapman and Cutler; Matt Fabian, managing director of Municipal Market Advisors; Keith Brainard, research director of the National Association of State Retirement Administrators; and Joshua Rauh, associate professor of finance at the Kellogg School of Management at Northwestern University — are expected to question whether pension plans are in crisis or state bankruptcy protection makes sense. Spiotto recently noted that Congress did not provide localities with the ability to declare bankruptcy until roughly 4,000 defaults occurred during the Great Depression. Robert Brennan case could be reopened after trust is found in Bahamas.

The Creditor of My Creditor Is My . . . Friend? What rights do holders of securitized debt have to participate in a bankruptcy case?

AmericanWest Bancorporation’s recent bankruptcy sale of equity it held in a subsidiary bank has been trumpeted as a novel solution to overcome barriers to recapitalization and reorganization of failing banks. The tools that made the AmericanWest reorganization successful, however, are the traditional tools of chapter 11 – namely, using chapter 11, particularly a sale under section 363 of the Bankruptcy Code, to avoid consents that would be required outside of bankruptcy. Although commentators on the case have suggested otherwise, the result is not extraordinary – a debtor may use section 363 to sell property of the estate even over the objection of creditors. The attention the case has received simply by using section 363 is, therefore, somewhat surprising. The objecting parties, however, were not direct creditors of AmericanWest and, in fact, were not even direct holders of the TruPs.

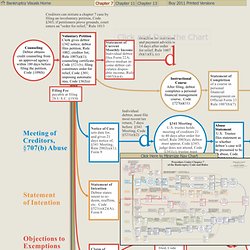

LoPucki's Bankruptcy Procedure Charts. Click Here to Minimize Nav Chart Bankruptcy Visuals HomeChapter 7Chapter 11Chapter 13Buy 2011 Printed Versions Please Wait . . .

Click and Drag the Chart. U.S. Trustee Program/Dept. of Justice. DE_Wisconsin. Welcome to $10 Debtor Education. A scary scenario: What if a U.S. state defaults? It's the year 2013.

A large U.S. state can't come up with the cash to make a bond payment. A default would ricochet through markets worldwide. What happens next? That's the scenario that a high-powered panel gathered to address this week at a conference in New York. Lifestyles of the Rich & Famous: Foreclosure Edition - Developments. Bank Lawyer's Blog: We Earn Money The Old-Fashioned Way: We Steal It. I'm not sure whether to be comforted or discouraged by the news that Interthink's Quarterly Fraud Risk Review Index shows that while mortgage fraud remains "substantially unchanged" last quarter when compared to the second quarter of this year (and is down from last year), the nature of the fraud has changed.

In the recent past, much mortgage fraud was perpetrated by bad actors in the mortgage business, sometimes crooked brokers (mortgage and real estate), appraisers, investors, "straw men and women," and even (The Horror! The Horror!) Lawyers, and sometimes by "professional crooks" who learned the fine art of mortgage fraud behind bars. In the third quarter of 2010, however, it appears we've returned to those days of yesteryear when men were men, women were women, and Johnny Cash was a boy named "Sue," days when most mortgage fraud was the act of a couple of people just trying to grab their little piece of the American Pie: Mr and Ms. UCLA-LoPucki Bankruptcy Research Database (BRD)

Debt Settlement: Is The Cure Worse Than The Disease? Photo: quaziephoto Everyone knows the story.

Unemployment is up. FICO scores are down. QE2 a ‘Ponzi scheme,’ says Pimco’s Gross. By Deborah Levine, MarketWatch NEW YORK (MarketWatch) — The Federal Reserve’s highly anticipated plan to engage in quantitative easing to pump money into the economy is a “Ponzi scheme,” said Bill Gross, who manages the world’s biggest bond fund for Pimco.

The actions of the Fed, led by Chairman Ben Bernanke, will “likely signify the end of a great 30-year bull market in bonds and the necessity for bond managers and, yes, equity managers to adjust to a new environment,” he wrote in a commentary posted on Pimco’s website Wednesday. See Gross’s full commentary.