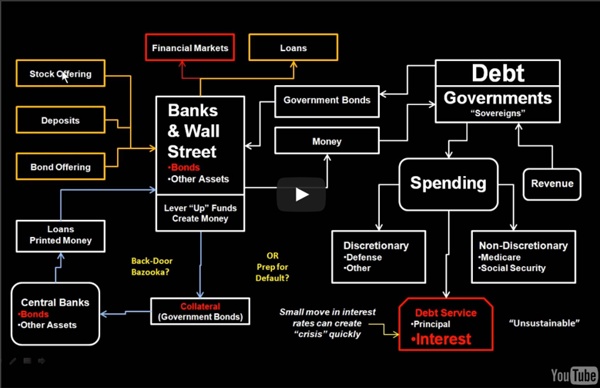

World debt comparison: The global debt clock The Corporation Welcome to YouTube! The location filter shows you popular videos from the selected country or region on lists like Most Viewed and in search results.To change your location filter, please use the links in the footer at the bottom of the page. Click "OK" to accept this setting, or click "Cancel" to set your location filter to "Worldwide". The location filter shows you popular videos from the selected country or region on lists like Most Viewed and in search results. Loading...

Europe According to Stereotype | andrewcusack.com A London-based graphic designer has created a series of maps depicting Europe according to the national stereotypes in the minds of various peoples. Yanko Tsvetkov, a Bulgarian living in Great Britain, created the first one in 2009 in the midst of the energy dispute between Russia and the Ukraine. Russia was labelled “Paranoid Oil Empire”, the Ukraine “Gas Stealers”, and the E.U. as “Union of Subsidized Farmers”. Switzerland was simply “Bank”. “I created the first one in 2009 because at that time there was an energy crisis in Europe,” Mr. Europe according to the French. Europe according to the Germans. Europe according to the Italians. Europe according to the British. Europe according to the Americans.

Outfoxed – Rupert Murdoch's War on Journalism Documentary | Watch Free Documentary Online “Outfoxed” examines how media empires, led by Rupert Murdoch’s Fox News, have been running a “race to the bottom” in television news. This documentary provides an in-depth look at Fox News and the dangers of ever-enlarging corporations taking control of the public’s right to know. The film explores Murdoch’s burgeoning kingdom and the impact on society when a broad swath of media is controlled by one person. Media experts, including Jeff Cohen (FAIR) Bob McChesney (Free Press), Chellie Pingree (Common Cause), Jeff Chester (Center for Digital Democracy) and David Brock (Media Matters) provide context and guidance for the story of Fox News and its effect on society. This documentary also reveals the secrets of Former Fox News producers, reporters, bookers and writers who expose what it’s like to work for Fox News.