Inside Story Americas - Has capitalism proven its durability? "American Pie in the Sky" by Nouriel Roubini. Exit from comment view mode. Click to hide this space NEW YORK – While the risk of a disorderly crisis in the eurozone is well recognized, a more sanguine view of the United States has prevailed. Modern American Economic History in a Few Charts. Matt Stoller is a fellow at the Roosevelt Institute.

You can follow him at The big economic strategy for the next term of whoever is Presidenti is essentially, “turn those machines back on”. It’s fracking to replace cheap oil and a new real estate bubble in housing. Essentially, the idea is to turn America into more and more of a resource extraction economy, or a petro-state. If American politics seems more and more oligarchical, that’s because the American political system is beginning to reflect the Middle Eastern oil states its economic investment implies it should. First, this is data showing investment in various investment sectors. World’s Most Prestigious Financial Agency – Called the “Central Banks’ Central Bank” – Slams U.S. Economic Policy.

The “Central Banks’ Central Bank” Slams the Federal Reserve The central banks’ central bank, the Bank of International Settlements or “BIS” – which is the world’s most prestigious mainstream financial body – has slammed the policy of America’s economic leaders. This is especially dramatic given that the banks own the Federal Reserve, and that the Federal Reserve and other central banks – in turn – own BIS. In other words, BIS is criticizing one of its main owners. Economics professor Michael Hudson notes: Paul Krugman has urged the Federal Reserve to simply lend banks an amount equal to their bad loans and negative equity (debts in excess of the market price of assets). For background, see this and this. Too Big Has Failed. Edward Lazear: The Worst Economic Recovery in History.

The Recovery According to Ed “We are not in a recession” Lazear. In Tuesday’s WSJ, Edward Lazear argued that we are now experiencing the “Worst Economic Recovery in History”.

Before dissecting this remarkable document, it would behoove the reader to recall that while he was Chair of George W. Bush’s Council of Economic Advisers, he stated unequivocally in May 2008 (also in the pages of the WSJ): “The data are pretty clear that we are not in a recession.” Is Obama Still on the Austerity Train? Mean-Spirited, Bad Economics. By Simon Johnson The principle behind unemployment insurance is simple.

Graphic of World Military Spending (Iran's too Small to Show up)

To sort... The Wyden-Ryan Plan for Health Care. Housing & Homeownership in America. Short-termism and the risk of another financial crisis. The truth is, some of us did see this coming.

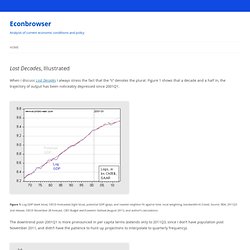

We tried to stop the excessive risk-taking that was fueling the housing bubble and turning our financial markets into gambling parlors. But we were impeded by the culture of short-termism that dominates our society. Our financial markets remain too focused on quick profits, and our political process is driven by a two-year election cycle and its relentless demands for fundraising. The 2007/8 financial crisis. Cognitive Regulatory Capture. Get Ready for TARP 2.0. Jobless Recoveries... I>Lost Decades</I>, Illustrated. When I discuss Lost Decades I always stress the fact that the “s” denotes the plural.

Figure 1 shows that a decade and a half in, the trajectory of output has been noticeably depressed since 2001Q1. Figure 1: Log GDP (dark blue), OECD forecasted (light blue), potential GDP (gray), and nearest neighbor fit against time, local weighting, bandwidth=0.3 (red). Source: BEA, 2011Q3 2nd release, OECD November 28 forecast, CBO Budget and Economic Outlook (August 2011), and author’s calculations. The downtrend post-2001Q1 is more pronounced in per capita terms (extends only to 2011Q3, since I don’t have population post November 2011, and didn’t have the patience to hunt up projections to interpolate to quarterly frequency).

Figure 2: Log per capita GDP (dark blue), potential GDP (gray), and nearest neighbor fit against time, local weighting, bandwidth=0.3 (red). Wall Street’s Euthanasia of Industry. Michael interviewed on Guns N Butter with Bonnie FaulknerListen here “When I was in Norway one of the Norwegian politicians sat next to me at a dinner and said, “You know, there’s one good thing that President Obama has done that we never anticipated in Europe.

He’s shown the Europeans that we can never depend upon America again. There’s no president, no matter how good he sounds, no matter what he promises, we’re never again going to believe the patter talk of an American President. Mr. Obama has cured us. The False Dichotomy of Greed. By Sell on News, a macro equities analyst.

American lessons in how to run a single currency. 20 July 2011, Financial Times In the 1990s, when European monetary union was a plan but not a reality, I would explain to students that the effect was to replace currency risk by credit risk.

With exchange rates free to float, loose monetary and fiscal policies would lead sooner or later to a fall in the exchange rate. That expectation implied higher interest rates. Currency markets would limit the scope for bad economic policies. Monetary union meant sovereign governments could no longer print money.

The Truth About the Economy. Financial Sector Fraud. The Billion-Dollar Bank Heist. OpenSecrets.org: Money in Politics. In U.S. Monetary Policy, a Boon to Banks. Note: The Trade is not subject to our Creative Commons license.

Rise in risk inequality helps explain polarized US voters. Public release date: 13-Jul-2011 [ Print | E-mail Share ] [ Close Window ] Contact: Philipp RehmRehm.16@osu.edu 614-292-8196Ohio State University COLUMBUS, Ohio – A new study of political polarization in the United States suggests that changes in the labor market since the 1970s has helped create more Republican and Democratic partisans and fewer independents. The growth in partisanship has to do with people's current income and – importantly – their expectations of job security, said Philipp Rehm, author of the study and assistant professor of political science at Ohio State University.

At one time, many voters were "cross-pressured" – when looking at what they earned now and their risks of losing that income, they felt torn between Republican and Democratic policies. In a study published recently in the British Journal of Political Science, Rehm estimated that slightly more than half of Americans could be counted as natural partisans in 1968, based on their income and job security. America: The Hungriest, Most Imprisoned Developed Country on Earth - Derek Thompson - Business. Fault Lines... The politics and economics of Austerity. Debating the future of capitalism - perspectives...

The ‘strong-dollar’ policy of the US. The impotence of monetary policy. In-depth analysis on Credit Writedowns Pro.

You are here: Economy » The impotence of monetary policy. Gross Echoes Buffett Saying Treasuries Have ‘Little Value’ on Debt, Dollar. Bill Gross, who runs the world’s biggest bond fund at Pacific Investment Management Co., said Treasuries “have little value” because of the growing U.S. debt burden. The U.S. has unrecorded debt of $75 trillion, or close to 500 percent of gross domestic product, counting what it owes on its bonds plus obligations for Social Security, Medicare and Medicaid, Gross wrote in his monthly investment outlook. The U.S. will experience inflation, currency devaluation and low-to- negative interest rates after accounting for consumer-price gains if it doesn’t reform its entitlement programs, he said.