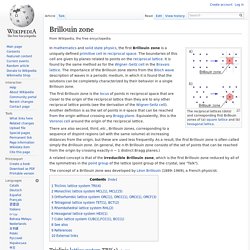

Pdf/physics/0106081.pdf. Information%20(Quantum)%20Mechanics%20-%20John%20L.%20Haller%20Jr.%20-%200106081. Physics notes.txt. Brownian motion via the Bernoulli process. An Algorithmic Introduction to Numerical Simulation of Stochastic Differential Equations : SIAM Review: Vol. 43, No. 3. Scientific Research Publishing. Brillouin zone. In mathematics and solid state physics, the first Brillouin zone is a uniquely defined primitive cell in reciprocal space.

The boundaries of this cell are given by planes related to points on the reciprocal lattice. It is found by the same method as for the Wigner–Seitz cell in the Bravais lattice. The importance of the Brillouin zone stems from the Bloch wave description of waves in a periodic medium, in which it is found that the solutions can be completely characterized by their behavior in a single Brillouin zone.

There are also second, third, etc., Brillouin zones, corresponding to a sequence of disjoint regions (all with the same volume) at increasing distances from the origin, but these are used less frequently. As a result, the first Brillouin zone is often called simply the Brillouin zone. The concept of a Brillouin zone was developed by Léon Brillouin (1889–1969), a French physicist.

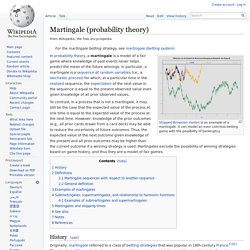

Triclinic lattice system TRI(4)[edit] See below for the aflowlib.org standard. See also[edit] Martingale (probability theory) Stopped Brownian motion is an example of a martingale.

It can model an even coin-toss betting game with the possibility of bankruptcy. To contrast, in a process that is not a martingale, it may still be the case that the expected value of the process at one time is equal to the expected value of the process at the next time. However, knowledge of the prior outcomes (e.g., all prior cards drawn from a card deck) may be able to reduce the uncertainty of future outcomes.

Thus, the expected value of the next outcome given knowledge of the present and all prior outcomes may be higher than the current outcome if a winning strategy is used. Martingales exclude the possibility of winning strategies based on game history, and thus they are a model of fair games. A basic definition of a discrete-time martingale is a discrete-time stochastic process (i.e., a sequence of random variables) X1, X2, X3, ... that satisfies for any time n, or which states that the average "winnings" from observation are 0. From Wolfram MathWorld.

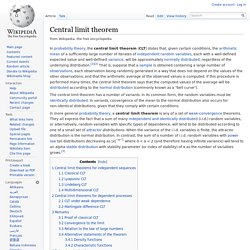

Central limit theorem. The central limit theorem has a number of variants.

In its common form, the random variables must be identically distributed. In variants, convergence of the mean to the normal distribution also occurs for non-identical distributions, given that they comply with certain conditions. In more general probability theory, a central limit theorem is any of a set of weak-convergence theorems. They all express the fact that a sum of many independent and identically distributed (i.i.d.) random variables, or alternatively, random variables with specific types of dependence, will tend to be distributed according to one of a small set of attractor distributions.

When the variance of the i.i.d. variables is finite, the attractor distribution is the normal distribution. Central limit theorems for independent sequences[edit] Classical CLT[edit] of these random variables. Lindeberg–Lévy CLT. Where Φ(x) is the standard normal cdf evaluated at x. Lyapunov CLT[edit] Lindeberg CLT[edit] Let be the i-vector.