Tp blockchain 5 theses en int. Fintech : "Le maître-mot doit être la libéralisation de la donnée" Selon le co-fondateur de l'agrégateur bancaire Budget Insight Clément Coeurdeuil, la nouvelle entité créée par l'AMF et l'ACPR pour encadrer les fintech est une "excellente nouvelle" qui devrait permettre au secteur de se développer davantage.

La décision de créer un guichet unique pour les Fintech est une excellente nouvelle. Concernant les agrégateurs – dont nous faisons partie – la décision de confier ce guichet à l’AMF et l’ACPR nous parait très cohérente. Lorsque les arbitrages sur la révision de la directive DSP2 auront été réalisés, ce sont les organismes nationaux qui distribueront les licences AIS et APS. Autrement dit, l’AMF et l’ACPR. Cet accord est très positif dans le sens où nous en tant qu’acteur du monde de la finance technologique, nous avons un intérêt très fort à ce que l’Etat, les banques et les sociétés de la fintech construisent un environnement sain et sécurisé. Les détails dans l'article de l'Agefi Quotidien consacré au sujet. Robo-advisor et financement participatif, les acteurs de la fintech en quête de reconnaissance. Etude sur le marche francais des Robo Advisors juil17. REGTech contre FINTech : au croisement entre réglementation et bouleversement sur le marché des titres - Actualités Asset Management.

Les services financiers sont l’un des secteurs les plus réglementés au monde.

C’est un secteur complexe où la réglementation influe sur la rapidité des changements et leur nature. Market Research Centre: Media centre - News. Robo-advisors are becoming an influential segment of the asset management industry.

One of the biggest changes on the horizon in the asset management sector is the integration of new technologies that are being used to make financial systems more efficient. In fact, the fintech landscape is heavily populated and more actors are walking onto the stage every day. All roads lead to fintech.

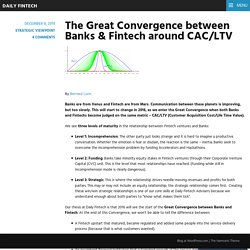

The fintech ecosystem is complex, and everyone seems to have a vested interest playing a role in its development. Blockchain & distributed ledgers : les banques d'investissement sont-elles prêtes ? The Great Convergence between Banks & Fintech around CAC/LTV. By Bernard Lunn Banks are from Venus and Fintech are from Mars.

Communication between these planets is improving, but too slowly. This will start to change in 2016, as we enter the Great Convergence when both Banks and Fintechs become judged on the same metric – CAC/LTV (Customer Acquisition Cost/Life Time Value). We see three levels of maturity in the relationship between Fintech ventures and Banks: Level 1: Incomprehension. 5 ways the Fintech revolution will reshape personal finance.

The Fintech revolution powered by Smart Data is happening.

Startups are disrupting financial technology that remained unchanged for decades. The new non-bank lenders adapt to emerging technologies and manage to integrate them into risk management, customer relationship management and pricing in order to enhance the service. WTF Is The Blockchain? Part II: How to send cryptocurrency and keep it safe. We have already learned the basics of the blockchain cryptocurrencies (like Bicotin) in WTF Is The Blockchain?

A Guide for Total Beginners. Cryptocurrency exists solely in digital, and the chain is completely decentralized, enabling it to never just “go down.” Transfers are verified by the hard work of miners, who add up all the numbers and solve mathematical equations to prove that the transfer is valid. Blocks of transactions are strung together, and include a summary, a time stamp, and proof of work. Thanks to the complicated equations and keys, the “public ledger” styled chain can never be wrong, and solved blocks can never be altered.

The unstoppable RoboAdvisor trend: Leapfrogging the independents. By Efi Pylarinou The Financial news focus in January was animated, colorful, and with 10 articles on Robo-Advisory.

As markets are in turmoil and portfolios are bleeding, most of us are questioning the impact of the macro-economic cycle. Last week Bernard Lunn shared his thoughts on the impact of the macro-economic cycle on Fintech startups and on Financial institutions. In a nutshell, incumbents and insurgents in financial services aren’t over-leveraged, so no blowup expected there.

Early stage startups can recover quickly from market shake-ups. January has not been boring on any front. The State of Robo Advisors — Personal Financial Advisor as a Service. The State of Robo Advisors — Personal Financial Advisor as a Service -By Vimarsh Karbhari & Chandra Inguva Robo advisor is an online wealth management service that provides automated, algorithm based portfolio management advice to retail investors.

How to survive the pre-bubble times in France? — Ventech Insight & Stories. Last week, a member of our team was pondering as to whether or not we should be attending the next First Tuesday session in London.

This single question suddenly brought me back 15 years in the past….. … back in 2000, the First Tuesdays was the place to be for a 25 year old French entrepreneur justifying to famous bankers why they should invest 10MF (!) In an idea they had come up with the day before…At that time, allegedly, the same entrepreneur would have been hosted in one of the many incubators located in the Sentier where he/she could have learned how to pitch investors in order to raise financing from funds that no longer exist or no longer would have invested in venture in France (Europ@web, Atlas Venture, 3i, Galileo partners…)! The current boiling of the French start-up ecosystem promises great optimism within a country which is clearly lacking of it. Banking Is Only The Start: 11 Big Industries Blockchain Tech Could Disrupt.

Banking and payments aren't the only industries that could be affected by blockchain tech.

Law enforcement, ride hailing, and charity also could be transformed. Bitcoin’s existence as a decentralized digital currency is made possible by what’s known as blockchain technology, essentially a public ledger that securely and automatically verifies and records a high volume of transactions digitally. Entrepreneurs have come to believe that more industries could be disrupted using this technology. There are plenty of business use cases for transactions that are verified and organized by a decentralized platform that requires no central supervision, even as it remains resistant to fraud. Banque Orange ou citrouille ? Articles liés. Fintech futures. Articles liés A report by the UK Government Chief Scientific Adviser. The UK Government's chief scientific advisor sets out ten recommendations for creating a sustainable national fintech ecosystem.

The report builds on the current work of HM Treasury and other parts of the Government to provide a longer-term vision for the UK fintech sector. Its recommendations are intended to provide a firm foundation to support and catalyse the growth of the sector out to 2025. In particular, it makes the case that the Government, regulators, business and academia must work together closely and in innovative ways. » Download the document below (PDF 68 pages) Blockchain: Powering the Internet of Value. Articles liés Seven years after the blockchain was invented, there is a shift in focus occurring in the discussion around the applications for the technology.

Previously, the discussion has focused mainly on the cryptocurrency known as Bitcoin. This year however, the attention has shifted more and more towards the core elements of the blockchain itself and how its nature as a distributed ledger for transactions could be leveraged. #mCal : Les événements startups à ne pas manquer en janvier. Everything You Wanted to Know About FinTech in Europe.

FinTech in Europe has never been more exciting. The continent’s ecosystem with innovative companies in emerging financial services has been a serious competition to the global financial industry giants with some of the most promising startups and FinTech “unicorns” coming from the region. Unicorns like Klarna, iZettle, Adyen, Funding Circle, TransferWise, POWA Technologies came from Europe as a proof of a strong standing of the market on a global arena.

According to Bloomberg, TechCrunch and Huffington Post, South East England is actually outpacing California on the number of jobs in FinTech along with rapidly growing funds and deals in the FinTech industry. Moreover, TechCrunch reported that European startups have raised more than $2.8 billion from VCs in Q2 2014, the highest quarterly total since the iconic dot-com bust in 2001. Clearly, European FinTech is creating a significant wave of competition for Silicon Valley and New York. What We Learned About the Wealth Management Industry Last Year. This article provides you with a flashback of the major touchpoints for the PFM/wealth management FinTech segment in 2015. Wealth management and PFM/personal money management solutions developed by the new-age FinTech have started to build scale. On the other hand, banks and financial services firms too have started to take note of this and have developed appropriate strategies to counter the threat.

Globally, there has been a trend of banks re-aligning their wealth management segments and focus. To a large extent, this trend was on account of regulations, associated costs and the new-age technology solutions. Banks have started to cater to wealth management/private banking services with a renewed focus. FINTECH: BANKS NEED TO PLAY CATCH-UP. Special Report | Banking Systems & Technology Keeping up with corporates’ increasingly sophisticated demands for more streamlined and well-integrated solutions is proving challenging. Technology is central to the modern treasurer’s toolkit.

“When it comes to good risk management—whether that is regulatory, operational or market-related—technology is at the core of our discussions with clients,” says Chris Jameson, head of corporate sales, Western Europe, at Bank of America Merrill Lynch. “It is an undisputed fact that technology facilitates greater visibility for treasury across business units and geographies, which is particularly important in light of regulatory risk and market uncertainty.” Britain’s quiet fintech revolution has begun – and we’re determined to back it. #FinTech : Ce que l'écosystème français peut retenir du Global Summit Innovate Finance.

Financial software design is being transformed by fintech. The startup revolution is changing paradigms in every industry including financial software. The term fintech was coined to refer to all companies providing financial services through technology. Fintech startups compete with established industry players in a fight where financial power is not the key differentiator. To set themselves apart, the smaller fintech players placed a bet on design and user experience, and as it turns out, it was a winning bet that helped them acquire and delight new customers. Credits to Charles Moldow from Foundation Capital. Full presentation here. As user-centric approaches to software development became more popular in the industry, design driven development became the norm , and software creation shifted from feature richness to simplicity. Digitisation replaces regulation as top concern for retail banks.

Retail banking priorities 2015 [Click to Enlarge] The need for a digital strategy has leapt to the top of retail banks’ agendas over the past year, replacing regulatory issues, as they look to fend of competition from tech and e-commerce rivals. FinTech Revolution: How Startups Are Changing Finance.

Morningstar UK adopts programmatic with Improve Digital. Behind the Fin Tech buzz. L’émergence des sociétés financières technologiques interroge les acteurs de la gestion de patrimoine. FINtech Focus: Fundbase Aims To Revolutionize Access To Hedge Funds. Finovate Europe 2015 : le palmarès. More than just ‘robo-advisors’ – digital entrants in wealth management. L’émergence des sociétés financières technologiques interroge les acteurs de la gestion de patrimoine.

FinTech Landscape. Investment Management, Online Financial Advisor. Investing Made Better. The easiest way to manage & improve your investments. Online Financial Advisor & Investing Advice. Olivier Goy lève 7 millions d'euros pour sa plateforme de prêts pour PME. Can Robo-Advisors Survive A Bear Market?