Effects of the Great Recession. This information is related to the effects of the Great Recession that is happening worldwide.

Overview[edit] The Great Recession was the worst post-World War II contraction on record:[1] Real gross domestic product (GDP) began contracting in the third quarter of 2008, and by early 2009 was falling at an annualized pace not seen since the 1950s.[2]Capital investment, which was in decline year-on-year since the final quarter of 2006, matched the 1957–58 post war record in the first quarter of 2009. The pace of collapse in residential investment picked up speed in the first quarter of 2009, dropping 23.2% year-on-year, nearly four percentage points faster than in the previous quarter.Domestic demand, in decline for five straight quarters, is still three months shy of the 1974–75 record, but the pace – down 2.6% per quarter vs. 1.9% in the earlier period – is a record-breaker already. Trade and industrial production[edit] Causes of the United States housing bubble. U.S.

Median Price of Homes Sold Government policies[edit] Housing tax policy[edit] In July 1978, Section 121 allowed for a $100,000 one-time exclusion in capital gains for sellers 55 years or older at the time of sale.[7] In 1981, the Section 121 exclusion was increased from $100,000 to $125,000.[7] The Tax Reform Act of 1986 eliminated the tax deduction for interest paid on credit cards. As mortgage interest remained deductible, this encouraged the use of home equity through refinancing, second mortgages, and home equity lines of credit (HELOC) by consumers.[8] The Taxpayer Relief Act of 1997 repealed the Section 121 exclusion and section 1034 rollover rules, and replaced them with a $500,000 married/$250,000 single exclusion of capital gains on the sale of a home, available once every two years.[9] This made housing the only investment which escaped capital gains.

Deregulation[edit] Starting in the 1980s, considerable deregulation took place in banking. Mandated loans[edit] Government policies and the subprime mortgage crisis. The U.S. subprime mortgage crisis was a set of events and conditions that led to a financial crisis and subsequent recession that began in 2008.

It was characterized by a rise in subprime mortgage delinquencies and foreclosures, and the resulting decline of securities backed by said mortgages. Several major financial institutions collapsed in September 2008, with significant disruption in the flow of credit to businesses and consumers and the onset of a severe global recession. Government housing policies, over-regulation, failed regulation and deregulation have all been claimed as causes of the crisis, along with many others. Credit rating agencies and the subprime crisis. Credit rating agencies (CRAs) — firms which rate debt instruments/securities according to the debtor's ability to pay lenders back — played a significant role at various stages in the American subprime mortgage crisis of 2007-2008 that led to the Great Recession of 2008-2009.

The new, complex securities of "structured finance" used to finance subprime mortgages could not have been sold without ratings by the "Big Three" rating agencies — Moody's Investors Service, Standard & Poor's, and Fitch Ratings. Impact on the crisis[edit] Credit rating agencies came under scrutiny following the mortgage crisis for giving investment-grade, "money safe" ratings to securitized mortgages (in the form of securities known as mortgage-backed securities (MBS) and collateralized debt obligations (CDO)) based on "non-prime"—subprime or Alt-A -- mortgages loans.

Subprime mortgage crisis. The U.S. subprime mortgage crisis was a set of events and conditions that were significant aspects of a financial crisis and subsequent recession that became manifestly visible in 2008.

It was characterized by a rise in subprime mortgage delinquencies and foreclosures, and the resulting decline of securities backed by said mortgages. These mortgage-backed securities (MBS) and collateralized debt obligations (CDO) initially offered attractive rates of return due to the higher interest rates on the mortgages; however, the lower credit quality ultimately caused massive defaults.[1] While elements of the crisis first became more visible during 2007, several major financial institutions collapsed in September 2008, with significant disruption in the flow of credit to businesses and consumers and the onset of a severe global recession.[2] When U.S. home prices declined steeply after peaking in mid-2006, it became more difficult for borrowers to refinance their loans. U.S. United States housing bubble. The United States housing bubble is an economic bubble affecting many parts of the United States housing market in over half of American states.

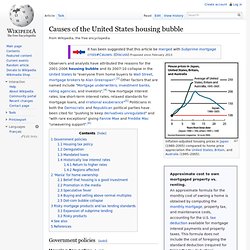

Housing prices peaked in early 2006, started to decline in 2006 and 2007, and reached new lows in 2012.[2] On December 30, 2008 the Case-Shiller home price index reported its largest price drop in its history.[3] The credit crisis resulting from the bursting of the housing bubble is — according to general consensus — the primary cause of the 2007–2009 recession in the United States.[4] Increased foreclosure rates in 2006–2007 among U.S. homeowners led to a crisis in August 2008 for the subprime, Alt-A, collateralized debt obligation (CDO), mortgage, credit, hedge fund, and foreign bank markets.[5] In October 2007, the U.S. Causes of the Great Recession. Many factors directly and indirectly caused the ongoing Great Recession (which started with the US subprime mortgage crisis ), with experts placing different weights upon particular causes. The crisis resulted from a combination of complex factors, including easy credit conditions during the 2002–2008 period that encouraged high-risk lending and borrowing practices; international trade imbalances; real-estate bubbles that have since burst; fiscal policy choices related to government revenues and expenses; and approaches used by nations to bail out troubled banking industries and private bondholders, assuming private debt burdens or socializing losses. [ 1 ] [ 2 ] One narrative describing the causes of the crisis begins with the significant increase in savings available for investment during the 2000–2007 period when the global pool of fixed-income securities increased from approximately $36 trillion in 2000 to $70 trillion by 2007.

The U.S. Financial crisis of 2007–08. The TED spread (in red) increased significantly during the financial crisis, reflecting an increase in perceived credit risk.

The financial crisis of 2007–2008, also known as the Global Financial Crisis and 2008 financial crisis, is considered by many economists the worst financial crisis since the Great Depression of the 1930s.[1] It resulted in the threat of total collapse of large financial institutions, the bailout of banks by national governments, and downturns in stock markets around the world. In many areas, the housing market also suffered, resulting in evictions, foreclosures and prolonged unemployment. In the immediate aftermath of the financial crisis palliative fiscal and monetary policies were adopted to lessen the shock to the economy.[19] In July 2010, the Dodd–Frank regulatory reforms were enacted in the U.S. to lessen the chance of a recurrence.[20] Background[edit] Share in GDP of U.S. financial sector since 1860[27] The U.S. Great Recession. This article is about the global economic downturn during the early 21st century.

For background on financial market events dating from 2007, see financial crisis of 2007–08. Financial crisis of 2007–08.