Germany: A False Model at Reports from the Economic Front. As growing numbers of countries face renewed austerity pressures, there is a tendency to explain the trend by searching for specific policy failures in each country rather than considering broader structural dynamics.

Key to the credibility of those who argue for a focus on national decisions is the existence of countries that people believe are performing well. Thus, the argument goes, if only policy makers followed best practices their people wouldn’t find themselves in such a bad place. Recently, German has become one of these model countries. Here is a typical framing of the German experience: At a time when unemployment rates in France, Italy, the UK, and the US are stuck around 8%-9%, many are turning to the apparent miracle in the German labor market in search of lessons.

A tale of two economies – Greece and Iceland. Last Friday (March 9, 2012), the Greek government effectively defaulted on its public debt after the required minimum of 75 per cent of private creditors agreed to the so-called “haircut” or debt swap.

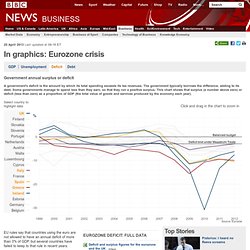

I find it amusing how the Euro leaders have attempted to massage the default as a debt swap or some other euphemism. The facts are obvious – close to 100 per cent of those who are holding Greek government debt will lose at a minimum 53.5 per cent of the value of their assets. This was forced on the private sector by the Troika (EU, ECB, and IMF) who apparently think it is preferable to undermine private sector wealth than introduce changes to their the Eurozone monetary system which might actually make it work! All the political elites in Europe (or most of them) seemed to be raising their Chardonnay glasses to toast a success. I only saw further failure in the deal. The causes: A very short history of the crisis. Europe’s youth generation – crushed by the euro austerity folly. Eurozone in crisis in graphics: Deficit. Continue reading the main story EU rules say that countries using the euro are not allowed to have an annual deficit of more than 3% of GDP, but several countries have failed to keep to that rule in recent years.

Note that Germany, Italy and France were all among the first countries to break the Maastricht rule during the last decade, while Spain and the Republic of Ireland ran surpluses before the 2008 crisis. Since 2008, peripheral economies such as Spain, Greece and Portugal have run big deficits, because their economies have slumped, generating less tax revenues and requiring more unemployment benefit payments. Ireland experienced an exceptionally enormous deficit of 31% of its GDP in 2010, largely due to the cost of rescuing its banks. Italy, however, has faired surprisingly well.

Spain. Greece.